ESOPs do it better?

Traditional leveraged buyouts operate on a simple (in theory) principle: purchase a business with as much debt as is feasible and use the business’ cash flow to pay it down. Even if the buyer does nothing to improve the overall value of the business, the reduction of debt in the capital stack increases equity value, providing a modest return on investment.

In the case of a widget factory, the LBO works flawlessly. Widget demand (especially in thought experiments) is stable, and the company will retain the value of its widget machines, widget distribution system, and widget sales contracts as debt is repaid over the next three to five years.

But as private equity (“PE”) has expanded, relatively easy wins (like widget factories) have become increasingly hard to find. Some funds have taken a Star Trek Enterprise approach: to explore strange new markets, seek out new alpha and new business models, and to boldly execute acquisitions where no fund has gone before.

Consider professional services companies, particularly those supporting the built environment (i.e. architecture, engineering, construction, environmental services or what we will refer to as “AEES”). When you close for the day at the widget factory, all the firm’s assets (e.g. the machines, the inventory, and the finished products) stay in the factory.

At an AEES firm, your assets get in their cars and go home. This risk is especially potent in the lower middle market space, where entire firms can be run by less than 30 employees and fewer than five partners who generate new business. Losing just two employees could evaporate 40% of the firm’s revenue, a potential death knell for a highly leveraged firm. Prospective investors must therefore heavily discount the value of the firm’s cash flows over and above market compensation for partners (if there is any) against the additional risk of employee exit.

Enter Employee Stock Ownership Plans (“ESOPs”). We have written before on the subject of ESOPs, their benefits, and their limitations (see ESOPs – A Different Angle, Spring 2018). An ESOP is a form of retirement plan that allows for a structure where employees are also the equity owners of the business. In the case of an ESOP-owned company, the assets still leave at the end of the day, but since the assets are also the owners, they have an incentive to remain connected to the company, which can expect to see them show up bright and early the next morning (or, in the case of Seattle, overcast and early). This structure reduces the risk of the post-transaction employee exit, and, given the inverse relationship of risk to value, should unlock additional value for ESOP owners that private equity cannot access. The ESOP structure even aligns with the low capital reinvestment requirements of the AEES industry. Incremental cash flow can go to repaying ESOP leverage or funding additional redemptions (primarily for retirements) since an architecture firm doesn’t have to worry about retaining significant cash & financing capacity to purchase a new widget machine. It’s no surprise that of the United States’ roughly 6,500 ESOPs, 19% are in professional or scientific services(1).

Maybe ESOPs did it better

Since an ESOP as a liquidity pathway theoretically has less transaction risk than exiting to private equity, we would expect to see ESOPs dominate the lower middle market of AEES M&A (where key man risk is the most prevalent), but not in the middle market and larger public space. After all, why should private equity hunt for transactions in an almost uniquely risky market? Historically, the data have shown this to be true. Between 2015 and 2020, 61% of total transaction volume for AEES firms under $10 million in revenue (i.e. the lower middle market) was to ESOPs(2). That figure was only 28% for firms with revenue between $10 million and $100 million (i.e. the middle market). For exits to PE (including both platforms and add-ons), those figures were 25% and 31% respectively.

So what? The market behaves exactly as you’d expect it to? Not exactly.

The market behaved like you’d expect it to.

By 2024, ESOP transaction volume for these businesses dropped from 61% to 25% of the lower middle market and from 28% to a barrel-scraping 4% of the middle market, while transaction volumes involving PE jumped to 62% and 84% respectively. Note that the number of transactions for ESOPs has stayed remarkably stable: 105 in 2021 and 107 as of Q3 2024. It’s likely that ESOPs have remained active at the small end of the lower middle market space, continuing relatively small transactions that PE is unwilling to pursue.

Private equity, on the other hand, went from 71 AEES transactions in 2021, to 186 transactions in Q3 2024, a 162% increase. What we’re seeing is an industry in the midst of radical transformation.

As PE transactions become increasingly common, competition between ESOPs and PE for potential acquisitions has become more likely. ESOPs are limited by available capital, lower internal hunger for M&A, and a complex regulatory structure that can hinder integration. Even more importantly, ESOPs are forced to underwrite acquisitions to a valuation limited by the maximum debt a business’ cash flow can service, rather than any specific value creation strategy, which limits check size for any given business. Meanwhile, PE firms are building platform companies that are highly efficient at purchasing and integrating small firms—machines custom-built for M&A. As platforms grow, they become increasingly able to diversify out the key man risk, a core advantage of ESOPs. As PE platforms become further normalized in the AEES space, key employees will have fewer options to jump ship.

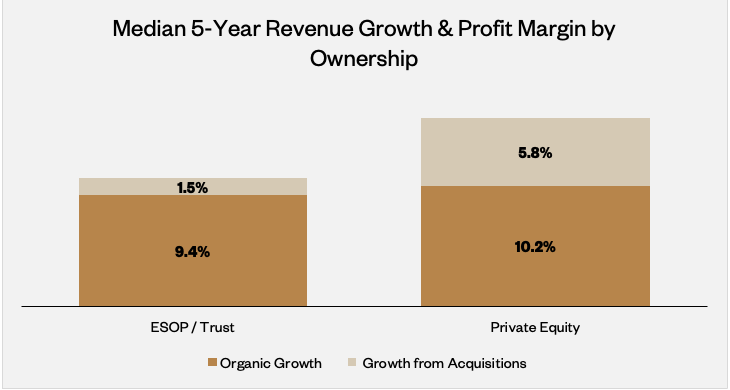

Profitability and revenue growth tell the same story. While AEES ESOPs generated median profit margins of 14.6% over the last five years, private-equity-owned AEES firms saw a notably higher margin at 18.0%, while also growing revenue at a faster rate over the same period.

The writing is on the wall. Private-equity-backed AEES firms are growing quicker, generating more profit, and acquiring more companies—even in the lower middle market space.

Good News for Middle Market AEES Owners

For an AEES owner, or group of owners, who may have previously expected that an ESOP was their only option for liquidity, this is welcome news. As we have discussed previously, the ESOP structure can expose shareholders to additional risk and reduce transaction gains, at least in the short term (see ESOP Myths and Realities, Spring 2002). Beyond shareholder value, ESOP structures often expose employees to concentration risks: effectively tying their income stream and retirement planning into a single firm’s performance. Finally, ESOPs are exposed to increased regulatory scrutiny, including Department of Labor and federal Employee Retirement Income Security Act oversight.

In 2018, when we last wrote on the risks of ESOPs, a business owner may fairly have asked “So what?”. Now, however, there are PE alternatives targeting the AEES space that can offer equal or better value, without exposing business owners to the risk inherent in an ESOP transaction. Sellers stand to benefit when there are more options available in the market. With the rise of PE activity across the AEES landscape, owners have more options than ever before, and should carefully weigh the alternatives against their personal objectives and the long-term growth goals of the business.

- National Center for Employee Ownership: Employee Ownership by the Numbers

- Data in this section is based on the 2024 State of the AEC Industry report by AEC Advisors, surveying 340 AEC firms